July 13, 2020

***Update***

The Small Business Cashflow (loan) Scheme has been extended until the end of 2020. Applications opened on 12 May 2020 and can now be submitted up to and including 31 December 2020.

After a disappointing response from banks in regards to COVID-19, the government has announced that they will provide interest free loans for a year to small businesses impacted by the COVID-19 economic shock to support their immediate cashflow needs and meet fixed costs. This is known as the Small Business Cashflow (Loan) Scheme (SBCS).

In summary:

Eligible Business and Organisations:

NB: Commonly owned groups of business and organisations will be treated as a single firm when applying the eligibility cap of 50 full-time-equivalent employees and for the purposes of assessing the available loan amount.

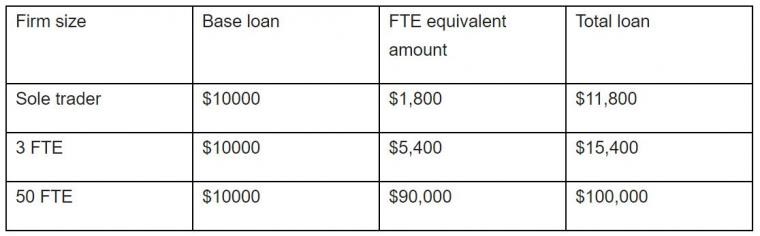

The SBCS:

Example below:

Applying for the SBCS:

In order to apply for the SBCS, as well as accepting usual T & C’s from the IRD, you will also need to confirm the following:

The process is going to administered by the IRD, and they will be taking applications on-line from 12 May 2020 to 31 December inclusive. To apply for the Loan you will need a MYIR account AND your business must have an NZBN number. If your organisation does not have an NZBN number you will need to obtain one first. Companies and organisations that already appear on a government register should already have an NZBN number, however if you are a sole trader, trust or partnership you will more than likely need to apply. You can apply here.

Please don’t hesitate to get in touch with your dpa expert to discuss your needs, we can help you decide whether an interest free loan is going to benefit your business, keeping in mind the operative word “loan” as this will need to be paid back. At this stage, we are unable to apply for the SBCS on behalf of our clients, but we can assist you with the process and answer any questions you may have.

You can read the full information from the IRD website here.